This video moves me to tears.

I learned of it from the creator who very kindly emailed me saying: "This is not meant as a political statement, but rather as an attempt to put a face on something that so often appears academic." And although a picture is not an argument, it is crucial that we keep in touch with the very real and profound effects that ideas, events and policies have on the lives of individual human beings. Art helps tremendously in that task and thus is an essential complement to intellectual debate.

People are the reason it all matters. Here's a look at a few of our faces.

from the email:

I see that you often embed youtube videos on your blog. I think you may be interested in "Pennyland - Echoes of the Great Depression" which I created from an original song written by my brother.

I've also placed it on my website at http://www.pennyland.org/

I thank you. In hard times artists, as much as anyone, need strong advocates to help share their work.

--Frank Thomas

.

Time to spend time with my family. Be back in about a week. This holiday season, I wish for you and your loved ones both spritual and material wealth, to be shared in an abundance of joy and peace.

Tuesday, December 23, 2008

Egalitarianism and Inflation

This article was recommended by a commenter. It's lengthy and not all of it is directly relevant to the topic of inflation. Also, although Rand has great ideas, her style of delivery can be distracting to those not already convinced of her point of view. For those reasons, I have chosen to post the excepts I found most pertinent to our current discussion on the nature of money.

excerpts from

by Ayn Rand

Agriculture is the first step toward civilization, because it requires a significant advance in men’s conceptual development: it requires that they grasp two cardinal concepts which the perceptual, concrete-bound mentality of the hunters could not grasp fully: time and savings. Once you grasp these, you have grasped the three essentials of human survival: time-savings-production. You have grasped the fat that production is not a matter confined to the immediate moment, but a continuous process, and that production is fueled by previous production. The concept of “stock seed” unites the three essentials and applies not merely to agriculture, but much, much more widely: to all forms of productive work. Anything above the level of a savage’s precarious, hand-to mouth existence requires savings. Savings buy time...

On a self-sustaining farm, your savings consisted mainly of stored grain and foodstuffs; but grain and foodstuffs are perishable and cannot be kept for long, so you ate what you could not save; your time-range was limited. Now, your horizon has been pushed immeasurably farther. You don’t have to expand the storage of your food: you can trade your grains for some commodity which will keep longer, and which you can trade for food when you need it. But which commodity? It is thus that you arrive at the next gigantic discovery: you devise a tool of exchange—money.

Money is the tool of men who have reached a high level of productivity and a long-range control over their lives. Money is not merely a tool of exchange: much more importantly, it is a tool of saving, which permits delayed consumption and buys time for future production. To fulfill this requirement, money has to be some material commodity which is imperishable, rare, homogeneous, easily stored, not subject to wide fluctuations of value, and always in demand among those you trade with. This leads you to the decision to use gold as money. Gold money is a tangible value in itself and a token of wealth actually produced. When you accept a gold coin in payment for your goods, you actually deliver the goods to the buyer; the transaction is as safe as simple barter. When you store your savings in the form of gold coins, they represent the goods which you have actually produced and which have gone to buy time for other producers, who will keep the productive process going, so that you’ll be able to trade your coins for goods any time you wish.

.

[Several paragraphs following describing what happens when people trade not with money representing saved production but money representing a promise of future production. Treated as equivalent, the increased amount of "money" gives the appearance of greater savings than actually exists and leads to unjustified increased risk taking, higher prices, and inappropriate consumption of real savings. The disconnection between money and production also allowed the development of the theory of a consumer-driven (as opposed to producer-driven) economy.]

Therefore, they conclude, the consumer—not the producer—is the motor of an economy. Let us extend credit, i.e., our savings, to the consumers—they advise—in order to expand the market for our goods.

But, in fact, consumers qua consumers are not part of anyone’s market; qua; consumers, they are irrelevant to economics. Nature does not grant anyone an innate title of “consumer”; it is a title that has to be earned—by production. Only producers constitute a market—only men who trade products or services for products or services. In the role of producers, they represent a market’s “supply”; in the role of consumers, they represent a market’s “demand.” The law of supply and demand has an implicit subclause: that it involves the same people in both capacities...

How many non-productive people could you support by your own effort? If the number were unlimited, if demand became greater than supply—if demand were turned into a command, as it is today—you would have to use and exhaust your stock seed... If you understand the function of stock seed--of savings--in a primitive farm community, apply the same principle to a complex industrial economy.

Wealth represents goods that have been produced, but not consumed. What would a man do with his wealth in terms of direct barter? Let us say a successful shoe manufacturer wants to enlarge his production. His wealth consists of shoes; he trades some shoes for the things he needs as a consumer, but he saves a large number of shoes and trades them for building materials, machinery and labor to build a new factory—and another larger number of shoes, for raw materials and for the labor he will employ to manufacture more shoes. Money facilitates this trading, but does not change its nature. All the physical goods and services he needs for his project must actually exist and be available for trade—just as his payment for them must actually exist in the form of physical goods (in this case, shoes). An exchange of paper money (or even of gold coins) would not do any good to any of the parties involved, if the physical things they needed were not there and could not be obtained in exchange for the money...

.

When a rich man lends money to others, what he lends to them is the goods he has not consumed. This is the meaning of "investment"... [C]redit means money, i.e. unconsumed goods, loaned by one productive person (or group) to another, to be repaid out of future production...

.

Consumption is the final, not the efficient, cause of production. The efficient cause is savings, which can be said to represent the opposite of consumption: they represent unconsumed goods. Consumption is the end of production, and a dead end, as far as the productive process is concerned. The worker who produces so little that he consumes everything that he earns, carries his own weight economically, but contributes nothing to future production. The worker who has a modest savings account, and the millionaire who invests his fortune (and all the men in between), are those who finance the future. The man who consumes without producing is a parasite, whether he is a welfare recipient or a rich playboy.

An industrial economy is enormously complex: it involves calculations of time, of motion, of credit, and long sequences of interlocking contractual exchanges. This complexity is the system’s great virtue and the source of its vulnerability. The vulnerability is psycho-epistemological. No human mind and no computer—and no planner—can grasp the complexity in every detail. Even to grasp the principles that rule it, is a major feat of abstraction. This is where the conceptual links of men’s integrating capacity break down...The most disastrous loss—which broke their tie to reality—is the loss of the concept that money stands for existing, but unconsumed goods...

----------------------------------------------------------------------------------------------

.

An economy based on specialization, division of labor and money is more complex than one based solely on direct barter, but the fundamental issues of production, consumption, saving and trade remain unaltered. Savings provide the escape from moment-to-moment survival, freeing up the time necessary for investments to improve future productivity. This investment in the future is only makes sense if our present and near-future are safe and secure. It is savings (production not consumed) that provides that security. To correctly calculate the extent of our safety-net, to decide how much excess production is available with which to take risks, or to tie up in future rather than immediate consumption, our money must provide an accurate accounting of that saving. The accuracy of that accounting is destroyed when "money" is disconnected from production such as occurs with money created by fiat. Money can fulfill its proper function only so long as it stands for actual existing goods--and this it does by remaining a good itself, i.e. a commodity-money.

.

Monday, December 22, 2008

Rule of Law vs. Regime Uncertainty

(Roberts' article is a bit dated on the specifics, but quite relevant on principle.)

Paulson's Faulty Imagination

By Russ Roberts

(This article appeared on NPR.org on 11/14/08)

Secretary Paulson might be the only person in America who worries that consumers haven't borrowed enough money. He says the consumer credit market has "ground to a halt." He wants to get it going again — maybe if we all just buy enough cars and use our credit cards, the economy will come back to life.

Paulson is also upset that banks aren't doing enough. He's given them all this money and they're sitting on it.

He doesn't seem to realize that these two phenomena are really one and the same.

He can inject all the money he wants into the consumer credit market and it isn't going to make us want to buy cars or use our credit cards.

We did enough of that for a while. More than enough. Too much. And right now, before we spend, spend, spend, we're going to wait and see if we keep our jobs.

But we're also going to wait and see what the government's going to do next. Nobody knows, and that evidently includes the secretary of the treasury.

When no one knows how the rules of the game are going to change — and they seem to change from week to week — who wants to take a risk? Who wants to borrow money? Who wants to invest? Business and consumers are hunkering down, waiting for the storm of change to pass.

The problem isn't liquidity.

It's uncertainty.

Paulson doesn't realize that his erratic attempts at creating liquidity are creating the uncertainty that makes liquidity meaningless.

And his erratic moves elsewhere just add to the uncertainty. A few days ago, he announced that he was "exploring strategies" to use the TARP (the Troubled Asset Relief Program) for "foreclosure mitigation." Then came the news that, no, the FDIC would have to go it alone in helping mortgage workouts. No TARP for them.

I guess he's done exploring. At least until tomorrow.

As the TARP spreads, the cost will keep rising. Remember the talk about how the government might even profit from its $700 billion "investment?" (Insert hollow laugh here.)

I'd feel better if the money spent so far was helping. But there's no evidence that it is achieving what Paulson intends.

And who's going to pay for all of this? Those who lived within their means, who went with the smaller house, who waited a few more years to get that new car, who took a part-time job rather than borrowing even more money to pay for college. Suckers. You missed out on the thrills and now you're going to be paying the bills. The prudent will be paying for the imprudent for a long time.

The great economist F.A. Hayek wrote that "the curious task of economics is to demonstrate to men how little they really know about what they imagine they can design."

With each improvisation, Secretary Paulson is proving how little he knows about what he imagines he can design.

Russell Roberts is professor of economics at George Mason University and a research fellow at Stanford's Hoover Institution. His latest book is The Price of Everything: A Parable of Possibility and Prosperity.

Another interesting article on this topic is one by Robert Higgs, "Regime Uncertainty: Why the Great Depression Lasted so Long and Why Prosperity Returned after the War." In this article, Higgs analyzes the economic effects of the New Deal and WWII on real standard of living. He clearly demonstrates economy did not recover (and prosperity did not return) until after the end of WWII. A key aspect the harmful effects of Hoover and FDR were the anti-business government policies and rhetoric which inhibited the resumption of private investment and delayed eventual recovery. Higgs also shows how arguments which credit WWII with ending the Great Depression are based on fatally flawed data. I read this article in an updated form published in Higgs' book Depression, War and Cold War, but the essentials of theory and data are in the pdf linked above.

Understanding the true effects of the New Deal policies is essential to formulating the best approach for the situation we face today. Many of the details between now and then are quite different, but the underlying principles of what leads to prosperity, and what are the effects government intervention, remain the same. As we hear more and more of the New New Deal, we better be sure we correctly understand the Old New Deal. For that, I recommend the works of Higgs, Freidman, Rothbard and Best.

On my desk sit library copies of The Great Crash of 1929 by John Kenneth Galbraith and The Return of Depression Economics by Paul Krugman which I hope I can get to before I run out of renewals. Anyone care to suggest other sources of opposing views?

.

Paulson's Faulty Imagination

By Russ Roberts

(This article appeared on NPR.org on 11/14/08)

Secretary Paulson might be the only person in America who worries that consumers haven't borrowed enough money. He says the consumer credit market has "ground to a halt." He wants to get it going again — maybe if we all just buy enough cars and use our credit cards, the economy will come back to life.

Paulson is also upset that banks aren't doing enough. He's given them all this money and they're sitting on it.

He doesn't seem to realize that these two phenomena are really one and the same.

He can inject all the money he wants into the consumer credit market and it isn't going to make us want to buy cars or use our credit cards.

We did enough of that for a while. More than enough. Too much. And right now, before we spend, spend, spend, we're going to wait and see if we keep our jobs.

But we're also going to wait and see what the government's going to do next. Nobody knows, and that evidently includes the secretary of the treasury.

When no one knows how the rules of the game are going to change — and they seem to change from week to week — who wants to take a risk? Who wants to borrow money? Who wants to invest? Business and consumers are hunkering down, waiting for the storm of change to pass.

The problem isn't liquidity.

It's uncertainty.

Paulson doesn't realize that his erratic attempts at creating liquidity are creating the uncertainty that makes liquidity meaningless.

And his erratic moves elsewhere just add to the uncertainty. A few days ago, he announced that he was "exploring strategies" to use the TARP (the Troubled Asset Relief Program) for "foreclosure mitigation." Then came the news that, no, the FDIC would have to go it alone in helping mortgage workouts. No TARP for them.

I guess he's done exploring. At least until tomorrow.

As the TARP spreads, the cost will keep rising. Remember the talk about how the government might even profit from its $700 billion "investment?" (Insert hollow laugh here.)

I'd feel better if the money spent so far was helping. But there's no evidence that it is achieving what Paulson intends.

And who's going to pay for all of this? Those who lived within their means, who went with the smaller house, who waited a few more years to get that new car, who took a part-time job rather than borrowing even more money to pay for college. Suckers. You missed out on the thrills and now you're going to be paying the bills. The prudent will be paying for the imprudent for a long time.

The great economist F.A. Hayek wrote that "the curious task of economics is to demonstrate to men how little they really know about what they imagine they can design."

With each improvisation, Secretary Paulson is proving how little he knows about what he imagines he can design.

Russell Roberts is professor of economics at George Mason University and a research fellow at Stanford's Hoover Institution. His latest book is The Price of Everything: A Parable of Possibility and Prosperity.

Another interesting article on this topic is one by Robert Higgs, "Regime Uncertainty: Why the Great Depression Lasted so Long and Why Prosperity Returned after the War." In this article, Higgs analyzes the economic effects of the New Deal and WWII on real standard of living. He clearly demonstrates economy did not recover (and prosperity did not return) until after the end of WWII. A key aspect the harmful effects of Hoover and FDR were the anti-business government policies and rhetoric which inhibited the resumption of private investment and delayed eventual recovery. Higgs also shows how arguments which credit WWII with ending the Great Depression are based on fatally flawed data. I read this article in an updated form published in Higgs' book Depression, War and Cold War, but the essentials of theory and data are in the pdf linked above.

Understanding the true effects of the New Deal policies is essential to formulating the best approach for the situation we face today. Many of the details between now and then are quite different, but the underlying principles of what leads to prosperity, and what are the effects government intervention, remain the same. As we hear more and more of the New New Deal, we better be sure we correctly understand the Old New Deal. For that, I recommend the works of Higgs, Freidman, Rothbard and Best.

On my desk sit library copies of The Great Crash of 1929 by John Kenneth Galbraith and The Return of Depression Economics by Paul Krugman which I hope I can get to before I run out of renewals. Anyone care to suggest other sources of opposing views?

.

Sunday, December 21, 2008

A short critque of government stimulus plans

This video clip briefly explains a part of the theory against government economic stimulus packages and touches on the empirical evidence which supports that theory. The speaker states that a govenment stimulus can not make the "economic pie" larger but only redistributes the slices. But the effect is much worse than that: a government redistribution plan necessarily makes the pie smaller for everyone. Not only does the government bureacracy use up a share (leaving a smaller pie to "redistribute"), but redistribution requires taking from the more efficient users of resources (i.e. those who procduce a greater surplus) and giving it to the less efficient users (those who either produce less or simply consume without producing.) As less surplus is produced, the pie keeps getting smaller. The long term effect of all "redistribution" efforts is the progressive erosion of productivity and wealth.

Saturday, December 20, 2008

How to turn a Recession into a Depression

An interesting article can be found at The Bear's Lair:

How recessions become Great Depressions

The author Martin Hutchinson looks at what was different about the recessions of 1921, 1947 and 1981 which were relatively mild and short, and compares what happened then to the Great Depression of 1929. From those comparisons, he then looks at our situation today and offers advice on the responses which will have the best chance of avoiding a depression and of keeping today's down-turn relatively mild and short.

Hopefully, the highly destructive effect of the Smoot-Hawley tariff are well understood won't be repeated, but without a correct understanding of the causes of the business cycle, other similarly harmful tactics by Congress and the Executive office could easily be enacted. As Robert Trasinski (TIA Daily, subscription required) points out, cap-and-trade could become the new Smoot-Hawley.

For even even further understanding of the economic events of the Great Depression, I recommend listening to the latest interview posted on EconTalk. Here's the description:

Robert Higgs, of the Independent Institute, talks with EconTalk host Russ Roberts about the Great Depression, the New Deal, and the effect of World War II on the American economy. Using survey results, financial data, and the pattern of investment in the 1930s, Higgs argues that New Deal policies created a climate of uncertainty that prolonged the Great Depression. Using consumption data, he argues that prosperity did not return during wartime, but rather after the war when government intervention in the economy subsided.

For a slightly different take, you might want to also listen to the interview with Rauchway:

Eric Rauchway of the University of California at Davis and the author of The Great Depression and the New Deal: A Very Short Introduction, talks with EconTalk host Russ Roberts about the 1920s and the lead-up to the Great Depression, Hoover's policies, and the New Deal. They discuss which policies remained after the recovery and what we might learn today from the policies of the past.

.

How recessions become Great Depressions

The author Martin Hutchinson looks at what was different about the recessions of 1921, 1947 and 1981 which were relatively mild and short, and compares what happened then to the Great Depression of 1929. From those comparisons, he then looks at our situation today and offers advice on the responses which will have the best chance of avoiding a depression and of keeping today's down-turn relatively mild and short.

Hopefully, the highly destructive effect of the Smoot-Hawley tariff are well understood won't be repeated, but without a correct understanding of the causes of the business cycle, other similarly harmful tactics by Congress and the Executive office could easily be enacted. As Robert Trasinski (TIA Daily, subscription required) points out, cap-and-trade could become the new Smoot-Hawley.

For even even further understanding of the economic events of the Great Depression, I recommend listening to the latest interview posted on EconTalk. Here's the description:

Robert Higgs, of the Independent Institute, talks with EconTalk host Russ Roberts about the Great Depression, the New Deal, and the effect of World War II on the American economy. Using survey results, financial data, and the pattern of investment in the 1930s, Higgs argues that New Deal policies created a climate of uncertainty that prolonged the Great Depression. Using consumption data, he argues that prosperity did not return during wartime, but rather after the war when government intervention in the economy subsided.

For a slightly different take, you might want to also listen to the interview with Rauchway:

Eric Rauchway of the University of California at Davis and the author of The Great Depression and the New Deal: A Very Short Introduction, talks with EconTalk host Russ Roberts about the 1920s and the lead-up to the Great Depression, Hoover's policies, and the New Deal. They discuss which policies remained after the recovery and what we might learn today from the policies of the past.

.

Thursday, December 18, 2008

It's all about money

I am taken aback that anyone could seriously think we can spend and consume our way to prosperity. I don’t get it. Seems so obvious to me that when you are over your head in debt, the solution is not more debt, but cutting back, letting go of sunk costs, reevaluating priorities, and saving up to recharge your safety net before taking on more risk. Yet... a plethora of seemingly intelligent, highly-educated individuals don’t share this point of view. (Imagine that - People don't agree with me!)

I am taken aback that anyone could seriously think we can spend and consume our way to prosperity. I don’t get it. Seems so obvious to me that when you are over your head in debt, the solution is not more debt, but cutting back, letting go of sunk costs, reevaluating priorities, and saving up to recharge your safety net before taking on more risk. Yet... a plethora of seemingly intelligent, highly-educated individuals don’t share this point of view. (Imagine that - People don't agree with me!)Where is the disconnect? How does something I see as so nonsensical make sense to anyone, let alone to well-intentioned, reasonable people?

One point of departure is how we think of money. What is money? What is its role in the economy? What is the proper relationship of government to money?

Before tackling which monetary policy will best address the problems we face today, we first need to explore the matter of money itself.

In the spirit of trying to understand the issues and differences in opinion as best as I possibly can, I have invited a guest to write a post for my blog. Glenn and I have been sporadically exchanging emails on economic matters since mid-October. His analysis and conclusions are Keynesian in origin, while mine start from an Austrian point of view. I have learned a lot from this exchange and greatly appreciate his willingness to trade explanations and ideas.

The better grasp I have of opposing arguments, the more refined is my thinking. I asked Glenn to write a post defending fiat money while I wrote one in support of a commodity money (i.e. a gold standard.) We each wrote our posts independently and “in the dark” with respect to the other’s points. We ended up taking slightly different tacks in addressing the issues. If he's willing, we can post follow ups considering the points the other raised which were not addressed in our original essays.

Please join the discussion. Let's keep to the subject of "What is (should be) money" and see what we can learn!

.

An argument for fiat money

(by guest writer, Glenn McIntosh)

Thanks to Beth for inviting me to post here. I have a lot of respect for what she's trying to do with this blog, and to invite open dialog so that we can all have a better understanding of the issues we're discussing.

In the interests of full disclosure, I'm an information technology professional with a background in Knowledge Management and a particular interest in Corporate Information Compliance, an increasingly important topic for most businesses and governmental organizations in the post-ENRON word. My interests extend to corporate finance, since that subject is at the core of how we design information systems for compliance. I also have a personal interest in Development Economics for emerging economies.

Having said all of that, Beth invited me to post my thoughts on the Gold Standard. I think that I understand a little bit about the audience for Beth's blog and the attendant sensibilities here, so where I can cite and contrast those views, I will (respectfully, of course).

For the scope of this discussion, I won't cover the cases for and against private currencies. From what I've been able to determine, many advocates of the Gold Standard are not necessarily advocates of replacing government agency-issued currency with private currencies, they mainly want to see our federal currency based on a commodity money system.

The original comment I made to Beth that caught her attention (and perhaps her ire) was my comment that all monies are basically belief systems, even commodity money. I don't just mean "belief" in the sense that when you and I make some sort of exchange that we both believe that we are getting something of worth. I also mean to imply that we believe that the managing entity (in this case, a governmental body), has a commitment to an expected system of valuation for the currency. This is true whether or not you have a fiat or a commodity money system. If your government is a credible steward of the money supply, you don't need the Gold Standard; and if it isn't, it won't be able to stay on it long anyway.

I think that readers of this blog would also vigorously support the notion that regardless of what type of currency system we happen to use, vigilance in regards to holding our elected officials accountable for their management of it is an inherent responsibility of citizenship. Again, this is true whether we're talking about fiat money or commodity money.

For backers of the Gold Standard, an important argument is that it is a defense against the government inflating the currency. They view this as a means whereby the government can impose arbitrary valuation on the currency and confiscate wealth, for starters. While this can be a real advantage of commodity money, it is dependent upon the belief that government adheres to the desired valuation policy. See my preceding points about this.

In regards to the basis of our discussion, the advantages of fiat currency that I support would naturally be the ones that readers here would have difficulty with.

For starters, a Gold Standard backed currency cannot do what a well-run fiat currency will do, that is to tailor the country's money supply to the economy's demand for currency. Gold supplies are dependent upon how much of the stuff can actually be dug up out of the ground. If supplies can't be found to keep pace with output and productivity, either the currency supply either has to be inflated, rendering invalid the touted advantage of the Gold Standard, held static or at a lower supply level, which causes a deflationary cycle to occur.

For example, let's say that you have $10,000 today and you intend to buy a car in the next few months. As output and productivity increase over those months, the money supply is held constant or fails to keep pace. This means that the available money must be allocated in increasingly smaller wages and prices to meet the demand of growing output and a growing workforce. The $10,000 purchase you intended to make a few months back is now a $9,000 purchase. If you wait a few months more, it will probably be an $8,000 purchase. You have more incentive to hang onto your currency, because its value will increase over time, not just for this purchase but for others affected by deflation. This is not just because you will be able to buy goods at lower prices, but once your money is spent, any new money you receive will be worth less and you will have incentive to hang onto this too, in the face of further falling prices and wages. In this type of environment, consumption and output decline and become a self-reinforcing loop. The result is the dreaded "liquidity trap".

There will come a point at which equilibrium is attained again, but this may take years and incur great financial hardships on those receiving decreasing wages or holding any debt (because they are having to pay an increasingly greater percentage of their money to service this debt as time goes on). We experienced such cycles in the 1800's and during the early years of the Great Depression.

Deflationary cycles in recent history have tended to be long, painful, and exaggerated in the absence of fiat currency. Some very strong arguments have been made that the countries that largely escaped the Great Depression of the 1930's were those that quickly abandoned the Gold Standard, and moved to a fiat currency in order to escape deflation. For a more detailed reading, Ben Bernanke and Harold James, detailed this in a paper called "The Gold Standard, Deflation, and Financial Crisis in the Great Depression: An International Comparison" published in 1991, by the National Bureau of Economic Research (NBER).

The 13 nations that abandoned the gold standard in 1931 experienced positive economic growth from 1932 on. The three countries that stuck with the Gold Standard through 1936 (France, Netherlands, and Poland) saw a 6% drop in industrial production in 1935, while the rest of the world was experiencing solid growth.

This is fundamental supply and demand economics, but it serves to depict in a simple sense the danger in unrestrained deflationary cycles. That's why modern industrial nations these days strive to manage their economies to sustain a 1-2% rate of inflation with monetary policy supported by the manipulation of a supply of fiat currency. In cycles of modest inflation, wages are rising (as are prices, but increasing productivity and efficiency, as well as advances in technology, can actually cause prices to fall in relation to wages – think of LCD TV or computer prices, for instance), and consumption rises.

Frankly, inflation can get out of hand with a poorly-managed fiat currency, due to a too rapidly-increased money supply. But a commodity money system is not immune to this either. If the supply of the commodity is sharply increased due to someone discovering a vast, new deposit of it under their land – inflation, due to increased supply of the commodity occurs. Additionally, nations with commodity-back money systems can also find themselves with their currency subject to speculative attacks, causing the price of gold to rise due to increased demand from those wanting to hoard gold during times of economic uncertainty.

There are other reasons that I'm not favorably disposed to the Gold Standard having to do with developing economies and the hardship that it imposes on them in terms of human suffering if they don't happen to have enough of the desired commodity buried underground, or cannot acquire it through trade with nations with commodity money, due to a lack of other natural resources. These countries tend to suffer disproportionately in terms of economic development, because what they really need is vigorous microeconomic activity to develop their educational, manufacturing, healthcare, and governmental infrastructures. They can only do this with the adoption of a currency system that is backed by production and output.

In short, as Beth mentioned, reasonable people with reasoned positions can still have fundamental disagreements about these types of issues. And in a real sense, there is enough history and data available to support a number of arguments of both parties. In each case here, I believe that we can all agree that irresponsible management on the part of a governing entity will render any well thought-out fiscal policy ineffective.

.

An argument for a commodity money

In a wonderful and informative email exchange I am having with an avowed Keynesian, we touched on the topic of the gold standard. He began his explanation on why he does not support a commodity money standard with:

I understand the attraction of commodity money in that it does provide a degree of predictability and stability in terms of inflation, and for those who see the current central banking structure as an inherently dangerous entity created on behalf of the federal government to control and confiscate wealth [Beth: That would be me] it offers a means to actually counter those activities. I don’t share those views.

Let’s start with the premise that any money system is a belief system, even one based on a supply of gold. Money only has the value that we assign it, the question is whether or not that value is based on our belief in the perpetual attractiveness and rarity of a precious metal or on the value of productivity and human capital.

The rest of his email follows quite logically from there, expressing concern that a gold standard would leave developing economies at a “decided disadvantage,” because they lack gold. Instead of gold, “these nations need money systems based on productivity and growth (fiat money) not on any particular commodity.”

I heartily agree that we all need money “based on productivity” but I heartily disagree that fiat money fits the bill.

Is money just whatever we choose to give value to? The experience of the past 37 years on a purely fiat money standard would seem to prove that paper is just as capable as gold in serving as a medium of exchange. But serving as a medium of exchange is only one of the essential functions of money, the other two are to serve as a store of value and as a standard of value.

So, what exactly is money? One way to get at the root of the issue is to ask: What are the facts of reality that give rise to the need for money?

When trade occurred on a very small, local level, direct barter was an adequate method of exchange. Increasing specialization and expanding division of labor led to the need for a "middle-man" commodity to serve as a common standard of value. People could then exchange their goods for this "middle commodity" and use it to trade for all other goods. This greatly enhanced the ease and flexibility of exchange. For the greatest utility, this "middle commodity" would have certain specific qualities.

In order to be confident that this "middle commodity" could be relied upon as a medium of exchange, it had to be valued by a sufficient number of other traders. As trade extended over greater distances, the commodity had to be portable and durable, of sufficient value (rarity) to serve for large transactions, and easily divisible to serve for small transactions. In dealing with strangers of unknown integrity, it was important for the exchange commodity to be difficult to counterfeit, of uniform quality and reliably pure.

This "middle commodity" is what we now call money. The commodity that best fit these objective requirements ended up being the precious metal gold. Before 1932, the U.S. primarily functioned on the gold coin standard. Subsequently, monetary policy evolved through various stages of decreasingly-redeemable paper notes until 1971 when Nixon officially defaulted on the gold standard, refusing to honor contractual agreements to pay our debts in gold. Since then, the value of our money has remained disconnected any commodity, and therefore, disconnected from the production of actual wealth. Instead, the volume and value of our currency is completely at the whim of politicians.

Much of the current debate over what government should do in response to recent economic events consists of how to direct those political whims. Money is no longer a measure and standard of wealth to use in trade but a political tool used to achieve political agenda. Should the Fed attempt to stimulate the economy through money creation or “allow” a market correction through money contraction? Should Congress attempt an economic boost with a stimulus package? If so, should the money go to private individuals, private businesses, or government projects? If to government projects, should the money support infrastructure, or prop up whichever struggling businesses politicians choose to support? Or should the government spend more to expand welfare payments? Should government attempt to create more consumer spending? Or, more investment spending? Or, should it create spending barriers so people and business will be more likely to build up reserves through saving and payment of debts?

The range of realistic and acceptable options for government action is partially defined by what is considered appropriate money. If fiat money is inappropriate, then all of the options involving the creation of more fiat money are disqualified. Easy or tight monetary policy, how to define the money supply (M1 or M2 or something else,) creation of money by "monetizing the debt" --all that is irrelevant if the whole idea of fiat money is fundamentally flawed.

Based on the primary functions of money, only a commodity money will maintain a stable and honest system.

Money is a medium of exchange.

Exchange of what? Goods and services. The results of the productive labor of one person for the results of the productive labor of another. Honest trade consists of the voluntary exchange of value for value. A commodity money keeps us bound to the fact that in order to obtain a value, you must offer an acceptable value in exchange. This is the essence of trade. Where do values come from? Productive labor. To exist, values must first be produced. It is possible to obtain values without offering an acceptable value in exchange. If done voluntarily, it is called charity. If done by force or fraud, it is called theft. Fiat money gives the appearance of exchanging value for value (production for production) but indistinguishably includes exchanges of nothing for something

Money is a store of value.

A commodity money is valued as a commodity itself. It both represents wealth and is wealth. A commodity money is wealth that is convenient and durable enough to last without a deterioration of quality or quantity and can therefore be stored for future use. Fiat money can be "stored for future use," but has no causal relationship to any real wealth. Fiat money only has value through government decree and enforcement. Commodity money is a store of value because it is a store of wealth - goods produced. Fiat money is not wealth, and therefore can not be a store of value. It does not represent any good produced, just laws passed.

Money is a standard of value.

Against this standard, we measure and express the value of all other goods and services. This comparison is truthful and useful only to the extent the standard is held constant. (Imagine the confusion and chaos if the length of the meter was subject to arbitrary change.) A commodity money is held constant through its relationship to an actual physical substance. Historically, the amount of new gold added each year has been dwarfed by the amount already in existence, and thus new gold has had minimal inflationary effect. There is no evidence that this ratio between new and existing gold stocks will change in the future. Additionally, once created, gold money essentially never goes out of existence, so a deflationary "contraction" can not occur.* In contrast, the value of fiat money is subject to arbitrary, political manipulation. The ability of governments to create and destroy money is essentially infinite. The value of money, as in all things, is subject to the law of supply and demand. As government creates (or withdraws) currency or reserves, the value of each unit will fall (or rise) thus destroying the "standard of value" function of money.

By allowing the government to create money without the prerequisite production of wealth that gives money its real value, fiat money enables one-sided transactions (theft, fraud, charity) to look like a fair exchange of values. The government attempts to create something from nothing, and then use its legal power to force us to accept that nothing in exchange for our productive efforts. Increasing the stock of fiat money does not create wealth. Instead, it expropriates the wealth created by others.

Historically, gold has been the most universal commodity money. In addition to meeting the requirements for a useful money (see above), gold is valued in and of itself. In a system of free money (as opposed to a system of legal tender) should gold no longer meet the requirements to serve as money (it becomes insufficiently rare or valuable as a commodity itself) a new commodity would gradually emerge as the preferred medium of exchange and measure of value. This evolution depends on traders being free to choose which commodity they prefer to accept in their exchanges, a freedom which is denied by legal tender laws.

As a culture and nation, we have come to understand the importance of freedom of choice in religious values, and our laws rigorously work to maintain the separation of Church and State. Production and trade are also expressions of value choices, and as such, deserve similar protections. One of the most fundamental of those protections is the legal support for an honest, stable money free of political manipulation. A money based on an objective standard with a physical existence independent of the desires of men: a commodity money, not a political money. A money based on voluntary exchange, not government fiat.

.

*This is true for a system of free banking and free currency which would result in 100% reserve banking--but that elaboration must wait for another day.

.

Image: 1957 Silver Certificate "one dollar in silver payable to the bearer on demand" - retrieved from my grandfather's piggy bank, along with silver coins.

.

Tuesday, December 16, 2008

Recommended Reading

A set of books recommended by Gene Epstein, former chief economist for the New York Stock Exchange and current economics editor at Barron's. You can put them on my Christmas list!!

HT fiatch

HT fiatch

The 10 Cannots

"The 10 Cannots " by William Boetcker (1873 – 1962)

You cannot bring about prosperity by discouraging thrift.

You cannot strengthen the weak by weakening the strong.

You cannot help little men by tearing down big men.

You cannot lift the wage earner by pulling down the wage payer.

You cannot help the poor by destroying the rich.

You cannot establish sound security on borrowed money.

You cannot further the brotherhood of man by inciting class hatred.

You cannot keep out of trouble by spending more than you earn.

You cannot build character and courage by destroying men's initiative and independence.

And you cannot help men permanently by doing for them what they can and should do for themselves.

(HT bblog)

You cannot bring about prosperity by discouraging thrift.

You cannot strengthen the weak by weakening the strong.

You cannot help little men by tearing down big men.

You cannot lift the wage earner by pulling down the wage payer.

You cannot help the poor by destroying the rich.

You cannot establish sound security on borrowed money.

You cannot further the brotherhood of man by inciting class hatred.

You cannot keep out of trouble by spending more than you earn.

You cannot build character and courage by destroying men's initiative and independence.

And you cannot help men permanently by doing for them what they can and should do for themselves.

(HT bblog)

Sunday, December 14, 2008

Differing Views on the Great Depression

For a measured and informative discussion on the economics and history of the Great Depression and the New Deal, take 35 minutes to watch video from the Canadian TV show, The Agenda.

Saturday, December 13, 2008

Market Success

from The Rational Capitalist:

No doubt we will continue to hear that "market failure" is to blame for the current crisis...The meltdown in the economy and particularly the automakers is, in fact, a glaring example of market success. When a company fails to make a profit and its stock plummets and no one will lend it money, it is the markets way of saying "stop what you are doing." If companies continue to produce products that no one wishes to buy would this be an example of market success or market failure?

.

Friday, December 12, 2008

A Change of Topic

U. S. Senate Minority Report:

More Than 650 International Scientists Dissent Over

Man-Made Global Warming Claims

Scientists Continue to Debunk “Consensus” in 2008

U.S. Senate Environment and Public Works Committee

Minority Staff Report (Inhofe)

www.epw.senate.gov/minority

Released: December 11, 2008

INTRODUCTION:

Over 650 dissenting scientists from around the globe challenged man-made global warming claims made by the United Nations Intergovernmental Panel on Climate Change (IPCC) and former Vice President Al Gore. This new 231-page U.S. Senate Minority Report report -- updated from 2007’s groundbreaking report of over 400 scientists who voiced skepticism about the so-called global warming “consensus” -- features the skeptical voices of over 650 prominent international scientists, including many current and former UN IPCC scientists, who have now turned against the UN IPCC. This updated report includes an additional 250 (and growing)scientists and climate researchers since the initial release in December 2007. The over 650 dissenting scientists are more than 12 times the number of UN scientists (52) who authored the media-hyped IPCC 2007 Summary for Policymakers.

The chorus of skeptical scientific voices grow louder in 2008 as a steady stream of peer-reviewed studies, analyses, real world data and inconvenient developments challenged the UN and former Vice President Al Gore's claims that the "science is settled" and there is a "consensus." On a range of issues, 2008 proved to be challenging for the promoters of man-made climate fears. Promoters of anthropogenic warming fears endured the following: Global temperatures failing to warm; Peer-reviewed studies predicting a continued lack of warming; a failed attempt to revive the discredited “Hockey Stick”; inconvenient developments and studies regarding CO2; the Sun; Clouds; Antarctica; the Arctic; Greenland; Mount Kilimanjaro; Hurricanes; Extreme Storms; Floods; Ocean Acidification; Polar Bears; lack of atmospheric dust; the failure of oceans to warm and rise as predicted.

In addition, the following developments further secured 2008 as the year the “consensus” collapsed. Russian scientists “rejected the very idea that carbon dioxide may be responsible for global warming”. An American Physical Society editor conceded that a “considerable presence” of scientific skeptics exist. An International team of scientists countered the UN IPCC, declaring: “Nature, Not Human Activity, Rules the Climate”. India Issued a report challenging global warming fears. International Scientists demanded the UN IPCC “be called to account and cease its deceptive practices,” and a canvass of more than 51,000 Canadian scientists revealed 68% disagree that global warming science is “settled.”

This new report issued by the Senate Environment and Public Works Committee's office of the GOP Ranking Member is the latest evidence of the growing groundswell of scientific opposition challenging significant aspects of the claims of the UN IPCC and Al Gore. Many scientific meetings are now being dominated by a growing number of skeptical scientists. The prestigious International Geological Congress, dubbed the geologists' equivalent of the Olympic Games, was held in Norway in August 2008 and prominently featured the voices of scientists skeptical of man-made global warming fears. [See Full report Here: & see: Skeptical scientists overwhelm conference: '2/3 of presenters and question-askers were hostile to, even dismissive of, the UN IPCC' ]

Even the mainstream media has begun to take notice of the expanding number of scientists serving as “consensus busters.” A November 25, 2008 article in Politico noted that a “growing accumulation” of science is challenging warming fears, and added that the “science behind global warming may still be too shaky to warrant cap-and-trade legislation.” Canada’s Financial Post noted on October 20, 2008, that “the number of climate change skeptics is growing rapidly.” New York Times environmental reporter Andrew Revkin noted on March 6, 2008, "As we all know, climate science is not a numbers game (there are heaps of signed statements by folks with advanced degrees on all sides of this issue)," Revkin wrote. (LINK) In 2007, Washington Post Staff Writer Juliet Eilperin conceded the obvious, writing that climate skeptics "appear to be expanding rather than shrinking.

Skeptical scientists are gaining recognition despite what many say is a bias against them in parts of the scientific community and are facing significant funding disadvantages. Dr. William M. Briggs, a climate statistician who serves on the American Meteorological Society's Probability and Statistics Committee, explained that his colleagues described “absolute horror stories of what happened to them when they tried getting papers published that explored non-‘consensus’ views.” Briggs, in a March 4, 2008, report, described the behavior as “really outrageous and unethical behavior on the parts of some editors. I was shocked.” (LINK) [Note: An August 2007 report detailed how proponents of man-made global warming fears enjoy a monumental funding advantage over skeptical scientists. LINK and a July 2007 Senate report detailing how skeptical scientists have faced threats and intimidation - LINK & LINK ]

(See the original report for the links.)

The 231 page report consists primarily of an annotated list of scientists whose views range from "skepticism to outright rejection of predictions of catastrophic man-made global warming." Credentials are listed along with a brief description of the scientists' views. Links are given but show up as a box with the URL as you roll over the highlighted text but do not take you directly to the relevant site.

I hope President-elect Obama's new environmental team takes the time to consider the these views, and then look carefully at the economic debacle of the EU cap-and-trade experiment before they make any decisions which will needlessly set our financial recovery back even further.

There are also lessons to be learned from the poor reviews the plan of the California Air Resources Board (CARB) received from the Legislative Analyst's Office and a peer-review report from a panel of economists.

.

Some different perspectives on some less commonly discussed aspects of the credit crisis

Here are a few good articles which address in depth various aspects of the current economic crisis. They are a bit long, but worth the time to expand your understanding.

Anatomy of a Train Wreck by Stan Liebowitz

Rather than sub-prime or prime status, Liebowitz shows that the more relevant factor in default rate for mortgages is adjustable vs. fixed interest rates.

Triple-A Failure by Roger Lowenstein

This article looks at the role the rating agencies played, including the potential for conflicts of interest, the existence adverse incentives and errors caused by the rating process itself. One aspect of the role of rating agencies this article does not stress is the lack of free market competition in the field of rating agencies. Regulatory control and certification by the S.E.C (through requiring and conferring "Nationally Recognized Statistical Rating Organization" status) leads to the destruction of competition for quality that all such government standard-setting causes.

An AP Stats Lecture by Arnold Kling

Here Kling uses the dilemma of needing to balance Type I and Type II statistical error as one of the factors leading to lending to borrowers with credit credit risk. This provides a more benign analysis of the alternatives faced in the mortgage loan process, rather than looking to vilify predatory lenders or deadbeat borrowers.

The Credit Crisis and Moral Hazards by Eugene Halloway

This article focuses on the moral hazards which occur when government interferes with the free market. While intending to provide protection and security, the actual effect of government regulation is something quite different.

The Greenspan Fed in Perspective by Roger Garrison

Includes some history of the Fed as well as explanations of and reasons for the shifts in post-1970's Fed monetary policy.

And for a novel idea on a possible solution to the problem: Let's try freedom!

The High Cost of Washington's Price Manipulation Policy by Yaron Brook and Don Watkins

.

Anatomy of a Train Wreck by Stan Liebowitz

Rather than sub-prime or prime status, Liebowitz shows that the more relevant factor in default rate for mortgages is adjustable vs. fixed interest rates.

Triple-A Failure by Roger Lowenstein

This article looks at the role the rating agencies played, including the potential for conflicts of interest, the existence adverse incentives and errors caused by the rating process itself. One aspect of the role of rating agencies this article does not stress is the lack of free market competition in the field of rating agencies. Regulatory control and certification by the S.E.C (through requiring and conferring "Nationally Recognized Statistical Rating Organization" status) leads to the destruction of competition for quality that all such government standard-setting causes.

An AP Stats Lecture by Arnold Kling

Here Kling uses the dilemma of needing to balance Type I and Type II statistical error as one of the factors leading to lending to borrowers with credit credit risk. This provides a more benign analysis of the alternatives faced in the mortgage loan process, rather than looking to vilify predatory lenders or deadbeat borrowers.

The Credit Crisis and Moral Hazards by Eugene Halloway

This article focuses on the moral hazards which occur when government interferes with the free market. While intending to provide protection and security, the actual effect of government regulation is something quite different.

The Greenspan Fed in Perspective by Roger Garrison

Includes some history of the Fed as well as explanations of and reasons for the shifts in post-1970's Fed monetary policy.

And for a novel idea on a possible solution to the problem: Let's try freedom!

The High Cost of Washington's Price Manipulation Policy by Yaron Brook and Don Watkins

.

Thursday, December 11, 2008

Blogger's Make a Difference

A story on the recent meaningful contributions of "econobloggers":

So you want to save the economy?

by Stephen Mihm

Boston Globe December 7, 2008

.

So you want to save the economy?

by Stephen Mihm

Boston Globe December 7, 2008

.

Wednesday, December 10, 2008

A few important bailout facts

Via Carpe Diem

From Dec. 1 WSJ editorial America's Other Auto Industry:

Consider labor costs. Take-home wages at the U.S. car makers average $28.42 an hour, according to the Center for Automotive Research. That's on par with $26 at Toyota, $24 at Honda and $21 at Hyundai. But include benefits, and the picture changes. Hourly labor costs are $44.20 on average for the non-Detroit producers, in line with most manufacturing jobs, but are $73.21 for Detroit (see chart below).

This $29 cost gap reflects the way Big Three management and unions have conspired to make themselves uncompetitive -- increasingly so as their market share has collapsed (see the chart below). Over the decades the United Auto Workers won pension and health-care benefits far more generous than in almost any other American industry. As a result, for every UAW member working at a U.S. car maker today, three retirees collect benefits; at GM, the ratio is 4.6 to one.

From a slightly different angle:

________________________________________________________

The chart [below](click to enlarge) is from the 2008 Harbour Report on automotive manufacturing productivity, showing the $606 per vehicle labor cost advantage for Toyota vs. the Detroit 3 in 2007, because of the average hourly labor rate of $75 for the Detroit 3 compared to the Toyota hourly rate of $47. Looking forward, Harbour predicts a labor rate of $54 per hour by 2011 for the Detroit 3, and only a $97 per vehicle cost disadvantage per vehicle.

Also:

GM sales in 2007: 9,370,000 vehicles

Toyota sales in 2007: 9,366,418 vehicles

GM profit/loss in 2007: -$38,730,000,000 (-$4,055 per car)

Toyota profit in 2007: +$17,146,000,000 (+$1,874 per car)

(from: Larry Kudlow and Sen. Tom Coburn on CNBC's "Kudlow & Company")

Lots more worth reading on Carpe Diem.

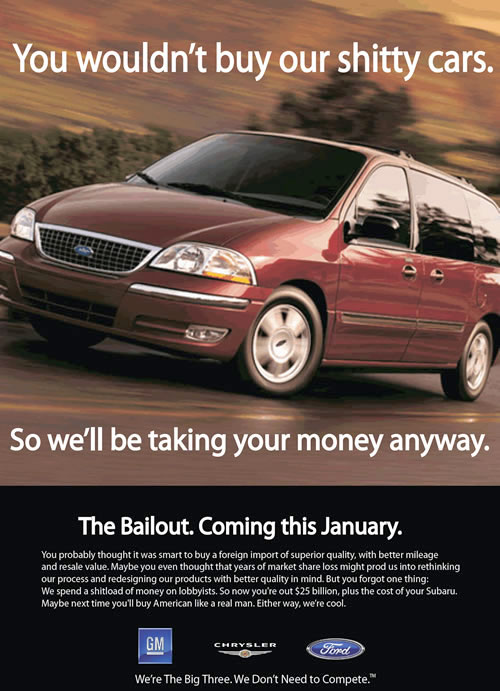

Humor is not only fun, it works because it carries a bit of truth. In the spirit of truth and humor: click here. (Warning to the sensitive: the language is blunt.)

.

Update: Another good article from back in Feb. 2006: "Against Toyota, GM Need to Mind the Gap" and a more recent one "Some companies are too pwerful to fail"

.

Update 12/12/08: Here's another: Bankruptcy Doesn't Equal Death

From Dec. 1 WSJ editorial America's Other Auto Industry:

Consider labor costs. Take-home wages at the U.S. car makers average $28.42 an hour, according to the Center for Automotive Research. That's on par with $26 at Toyota, $24 at Honda and $21 at Hyundai. But include benefits, and the picture changes. Hourly labor costs are $44.20 on average for the non-Detroit producers, in line with most manufacturing jobs, but are $73.21 for Detroit (see chart below).

This $29 cost gap reflects the way Big Three management and unions have conspired to make themselves uncompetitive -- increasingly so as their market share has collapsed (see the chart below). Over the decades the United Auto Workers won pension and health-care benefits far more generous than in almost any other American industry. As a result, for every UAW member working at a U.S. car maker today, three retirees collect benefits; at GM, the ratio is 4.6 to one.

From a slightly different angle:

________________________________________________________

The chart [below](click to enlarge) is from the 2008 Harbour Report on automotive manufacturing productivity, showing the $606 per vehicle labor cost advantage for Toyota vs. the Detroit 3 in 2007, because of the average hourly labor rate of $75 for the Detroit 3 compared to the Toyota hourly rate of $47. Looking forward, Harbour predicts a labor rate of $54 per hour by 2011 for the Detroit 3, and only a $97 per vehicle cost disadvantage per vehicle.

Also:

GM sales in 2007: 9,370,000 vehicles

Toyota sales in 2007: 9,366,418 vehicles

GM profit/loss in 2007: -$38,730,000,000 (-$4,055 per car)

Toyota profit in 2007: +$17,146,000,000 (+$1,874 per car)

(from: Larry Kudlow and Sen. Tom Coburn on CNBC's "Kudlow & Company")

Lots more worth reading on Carpe Diem.

Humor is not only fun, it works because it carries a bit of truth. In the spirit of truth and humor: click here. (Warning to the sensitive: the language is blunt.)

{kind=link}

.

Update: Another good article from back in Feb. 2006: "Against Toyota, GM Need to Mind the Gap" and a more recent one "Some companies are too pwerful to fail"

.

Update 12/12/08: Here's another: Bankruptcy Doesn't Equal Death

Tuesday, December 9, 2008

Economic Freedom of the World, 2008

As prosperity depends on freedom, this news is not encouraging.

from the Cato Policy Report Nov/Dec 2008

U.S. Falls to 8th in Economic Freedom Annual Report

from the Cato Policy Report Nov/Dec 2008

U.S. Falls to 8th in Economic Freedom Annual Report

Economic freedom remains on the rise around the world but has declined notably in the United States since the year 2000. That’s the blockbuster finding of the 2008 edition of the Economic Freedom of the World, an annual report co-published in the United States by the Fraser Institute and the Cato Institute.

In 2000, the United States was the second- freest economy in the world according to the report, written by economists James Gwartney of Florida State University and Robert Lawson of Auburn University. This year the United States has fallen to eighth place, behind Hong Kong (the perennial first-place finisher), Singapore, New Zealand, Switzerland, the United Kingdom, Chile, and—you heard it here first—Canada.

More significant than the United States’ drop in the rankings is its fall in the freedom ratings: on a scale of 0–10, the U.S. fell from 8.55 in 2000 to 8.04. Only five countries have experienced a greater decline over the same time period: Zimbabwe, Argentina, Niger, Venezuela, and Guyana.

The annual peer-reviewed report uses 42 different measures to create an index ranking of 141 countries around the world based on polices that encourage economic freedom. The cornerstones of economic freedom are personal choice, voluntary exchange, freedom to compete, and security of private property. Economic freedom is measured in five different areas: (1) size of government; (2) legal structure and security of property rights; (3) access to sound money; (4) freedom to trade internationally; and (5) regulation of credit, labor, and business.

Research shows that individuals living in countries with high levels of economic freedom enjoy higher levels of prosperity, greater individual freedoms, and even longer life spans.

You can order Economic Freedom of the World: 2008 Annual Report from the Cato bookstore at www.catostore.org or view it for free online at http://www.freetheworld.com/.

Monday, December 8, 2008

What's so great about the Great Depression?

As worries of a deepening recession loom before us, more and more comparisons are made between today and the Great Depression, looking for similarities and differences, examining the past like a crystal ball to the future. Bank failures and the stock market drop, though not as severe, are reminiscent of 1929. Are today’s losses going to last for decades? Are we headed for period of 20+% unemployment? What can we learn from that devastating time that will help us mitigate if not avoid the struggles and hardships suffered back then?

Fewer and fewer people are around who lived through those times, but still most of us have been touched in some way. My grandparents were born in 1902 putting them just at the beginning of their adult lives at the time of the stock market crash. Both went to college at the University of Illinois, graduating and getting married in 1926. My grandmother told stories of men (she called them hobos) who came to their back door asking for food, and then marking the house to alert others of their success or failure. My grandfather was able to enter a well established family business and though times were tight, was never without work and a house. Charity was a constant theme in his life. He lived to be 98, but has been gone for eight years now.

Fewer and fewer people are around who lived through those times, but still most of us have been touched in some way. My grandparents were born in 1902 putting them just at the beginning of their adult lives at the time of the stock market crash. Both went to college at the University of Illinois, graduating and getting married in 1926. My grandmother told stories of men (she called them hobos) who came to their back door asking for food, and then marking the house to alert others of their success or failure. My grandfather was able to enter a well established family business and though times were tight, was never without work and a house. Charity was a constant theme in his life. He lived to be 98, but has been gone for eight years now.

My father-in-law was born in 1918. The depression permeated his childhood. Orphaned while not yet through college, and unable to make the payments, he and his two brothers simply packed up and walked away from their family home. He recalls the New Deal as providing jobs when there otherwise were none. This summer we celebrated his 90th birthday, and the memories of the hard times are still sharp.

My father-in-law was born in 1918. The depression permeated his childhood. Orphaned while not yet through college, and unable to make the payments, he and his two brothers simply packed up and walked away from their family home. He recalls the New Deal as providing jobs when there otherwise were none. This summer we celebrated his 90th birthday, and the memories of the hard times are still sharp.

My dad, born in 1925, grew up in Chicago in a family which squeaked by. His tales include Sunday suppers consisting of popcorn and apples, as two big meals a day just wasn’t possible. His first job put him on a ship to Europe and in a tank under Patton. His memories of scarce resources morphed into lessons of frugality and self-reliance which he passed on to his five daughters. Turn out the lights. Two squares of toilet paper should be enough. His delight in a flat-tipped spoon designed to get the last little bit of peanut butter out of the jar. He’s healthy and going strong in his early 80’s, enjoying the fruits of his successful entrepreneurship, still fiscally prudent and an enthusiastic advocate of conservation.

My dad, born in 1925, grew up in Chicago in a family which squeaked by. His tales include Sunday suppers consisting of popcorn and apples, as two big meals a day just wasn’t possible. His first job put him on a ship to Europe and in a tank under Patton. His memories of scarce resources morphed into lessons of frugality and self-reliance which he passed on to his five daughters. Turn out the lights. Two squares of toilet paper should be enough. His delight in a flat-tipped spoon designed to get the last little bit of peanut butter out of the jar. He’s healthy and going strong in his early 80’s, enjoying the fruits of his successful entrepreneurship, still fiscally prudent and an enthusiastic advocate of conservation.

So now to my generation. We too have been touched by the Great Depression through its imprints on our parents and grandparents. Their stories have a poignancy sharpened by our shared lives, yet blurred by the fact we are looking through someone else’s eyes. We too feel the concern and worry of experiencing such times of tenuousness and uncertainty. So we peer closely, looking for clues, for understanding, and hopefully for guidance and answers.

The Great Depression was a turning point in economic thought as well in personal philosophy. I don’t think I can capture the shift better than this summary by Mark Skousen:

So which model is right? Communism and socialism were embraced earlier this century as potential answers, but the devastating experience of the Soviet experiment has shown those paths lead to tyranny and impoverishment. We now are trying to decide once again between laissez-faire capitalism and a Keynesian-style mixed-economy. How shall we decide? What exactly are these two systems of economic theory? Where are they similar? Where do they part ways? How do we decide which is right, or at least which is best?

This is my current intellectual journey which I try to share on this blog. My basic assumption is that most people are honest and caring, wanting to find solutions which are both practical and just. Yet while we are searching, we come to such different conclusions. What exactly are the points of divergence? If we can’t convince one another, can we at least better understand how and why we differ?

So much is riding on the answers we choose. Can we keep in mind that, for the most part, we are on the same side, each doing our best to grapple with complexities that have such immediate and immense effects on our one and only life? That is my goal. I hope you will join me.

Skousen, Mark, "The Great Depression" in The Elgar Companion to Austrian Economics, ed. Peter Boettke, Edward Elgar Pub. Ltd., 1994

.

{kind=link}

Fewer and fewer people are around who lived through those times, but still most of us have been touched in some way. My grandparents were born in 1902 putting them just at the beginning of their adult lives at the time of the stock market crash. Both went to college at the University of Illinois, graduating and getting married in 1926. My grandmother told stories of men (she called them hobos) who came to their back door asking for food, and then marking the house to alert others of their success or failure. My grandfather was able to enter a well established family business and though times were tight, was never without work and a house. Charity was a constant theme in his life. He lived to be 98, but has been gone for eight years now.

Fewer and fewer people are around who lived through those times, but still most of us have been touched in some way. My grandparents were born in 1902 putting them just at the beginning of their adult lives at the time of the stock market crash. Both went to college at the University of Illinois, graduating and getting married in 1926. My grandmother told stories of men (she called them hobos) who came to their back door asking for food, and then marking the house to alert others of their success or failure. My grandfather was able to enter a well established family business and though times were tight, was never without work and a house. Charity was a constant theme in his life. He lived to be 98, but has been gone for eight years now.{kind=link}

My father-in-law was born in 1918. The depression permeated his childhood. Orphaned while not yet through college, and unable to make the payments, he and his two brothers simply packed up and walked away from their family home. He recalls the New Deal as providing jobs when there otherwise were none. This summer we celebrated his 90th birthday, and the memories of the hard times are still sharp.

My father-in-law was born in 1918. The depression permeated his childhood. Orphaned while not yet through college, and unable to make the payments, he and his two brothers simply packed up and walked away from their family home. He recalls the New Deal as providing jobs when there otherwise were none. This summer we celebrated his 90th birthday, and the memories of the hard times are still sharp. My dad, born in 1925, grew up in Chicago in a family which squeaked by. His tales include Sunday suppers consisting of popcorn and apples, as two big meals a day just wasn’t possible. His first job put him on a ship to Europe and in a tank under Patton. His memories of scarce resources morphed into lessons of frugality and self-reliance which he passed on to his five daughters. Turn out the lights. Two squares of toilet paper should be enough. His delight in a flat-tipped spoon designed to get the last little bit of peanut butter out of the jar. He’s healthy and going strong in his early 80’s, enjoying the fruits of his successful entrepreneurship, still fiscally prudent and an enthusiastic advocate of conservation.

My dad, born in 1925, grew up in Chicago in a family which squeaked by. His tales include Sunday suppers consisting of popcorn and apples, as two big meals a day just wasn’t possible. His first job put him on a ship to Europe and in a tank under Patton. His memories of scarce resources morphed into lessons of frugality and self-reliance which he passed on to his five daughters. Turn out the lights. Two squares of toilet paper should be enough. His delight in a flat-tipped spoon designed to get the last little bit of peanut butter out of the jar. He’s healthy and going strong in his early 80’s, enjoying the fruits of his successful entrepreneurship, still fiscally prudent and an enthusiastic advocate of conservation.So now to my generation. We too have been touched by the Great Depression through its imprints on our parents and grandparents. Their stories have a poignancy sharpened by our shared lives, yet blurred by the fact we are looking through someone else’s eyes. We too feel the concern and worry of experiencing such times of tenuousness and uncertainty. So we peer closely, looking for clues, for understanding, and hopefully for guidance and answers.

The Great Depression was a turning point in economic thought as well in personal philosophy. I don’t think I can capture the shift better than this summary by Mark Skousen:

The Great Depression of the 1930s was the most traumatic economic event of the twentieth century. It was especially shocking when one considers the great advances that had been achieved in Western living standards since the turn of the century. The economic abyss represented a watershed in economic history and theory; its effects on attitudes and policies still linger at this dawn of a new century.

The brunt of the depression was felt in 1929-33. In the USA, industrial output fell by over 30 per cent. Nearly half the commercial banks failed. The unemployment rate soared to 25 per cent. Stock prices lost 88 per cent of their value. Europe and the rest of the world experienced similar turmoil. In addition, the recovery in the 1930s was slow and uneven; unemployment remained high (above 15 per cent) until the armament race heated up in the early 1940s. The prolonged depression created an environment critical of laissez-faire policies and favorable towards ubiquitous state interventionism throughout the Western world. It led to the Welfare State and boundless faith in Big Government. It caused most of the Anglo-American economics profession to question classical free-market economics and to search for radical anti-capitalist alternatives, eventually converting to the 'new economics' of Keynesianism and 'demand-side' economics. Prior to the Great Depression, most Western economists accepted the classical virtues of thrift, limited government, balanced budgets, the gold standard and Say's Law. While most economists continued to defend free enterprise and free trade on a microeconomic scale, they rejected traditional views on a macroeconomic level in the postwar period, advocating consumption over saving, fiat money over the gold standard, deficit spending over a balanced budget and active state interventionism over limited government. They bought the Keynesian argument that a free market was inherently unstable and could result in high levels of unemployed labor and resources for indefinite periods. They blamed the Great Depression on laissez-faire capitalism and contended that only massive government spending during the Second World War saved the capitalist system from defeat. In short, the depression opened the door to widespread collectivism in the USA and around the world. * (emphasis mine)